The delinquency rate for mortgage loans on one-to-four-unit residential properties decreased to a seasonally adjusted rate of 5.3% of all loans outstanding at the end of the second quarter of 2015, according to the Mortgage Bankers Association.

This was the lowest level since the second quarter of 2007. The delinquency rate decreased 24 basis points from the previous quarter, and 74 basis points from one year ago.

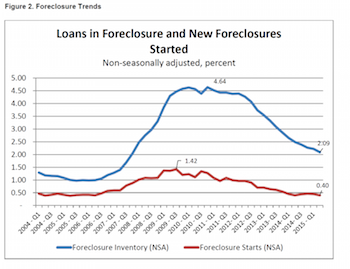

The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the second quarter was 2.09%, down 13 basis points from the first quarter and 40 basis points lower than the same quarter one year ago.

(Source: Mortgage Bankers Association)

This was the lowest foreclosure inventory rate since the fourth quarter of 2007.

“It is not surprising that incidences of mortgage payment difficulties are falling to back to historical norms. Despite edging-up over the second quarter, mortgage interest rates are still very low by the standards of the past 20-30 years,” says Ed Stansfield, chief property economist for Capital Economics. “And with house prices currently rising by 5% to 6% year-over-year, the number of mortgages that are underwater will have seen further declines. Admittedly, job creation has slowed since the start of the year, and the unemployment rate was unchanged in July. But overall the economy is still creating jobs at a steady rate, supporting mortgage borrowers.

“The downward trend in borrowers experiencing payment difficulties should continue, as unemployment sees further declines and mortgage rates only increase gradually. In turn, that should increase lenders’ willingness to extend mortgage credit, providing further support to the recent increase in housing market activity,” Stansfield says.

The percentage of loans on which foreclosure actions were started during the second quarter was 0.4%, a decrease of five basis points from the previous quarter. The foreclosure starts rate was unchanged relative to the second quarter of 2014.

The serious delinquency rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 3.95%, a decrease of 29 basis points from the previous quarter, and a decrease of 85 basis points from the second quarter of 2014. This was the lowest level since the fourth quarter of 2007.

“Overall delinquency rates and the percentage of loans in foreclosure continued to fall in the second quarter and are at their lowest levels since 2007,” says Marina Walsh, MBA’s Vice President of Industry Analysis. “Even more telling, nearly every state in the nation reported declining foreclosure inventory rates over the second quarter, reflecting a nationwide housing market recovery and strong job market that provide opportunities for distressed loans to be resolved rather than be put into foreclosure.

“The overall delinquency rate for FHA loans dropped to 9.01% in the second quarter from 9.1%, as the 90 day or more delinquent category declined. However, the 30-day and 60-day delinquency rate was up by a combined 10 basis points from the previous quarter,” she says. “In addition, the FHA foreclosure inventory rate rose to 2.68% in the second quarter, four basis points higher than the previous quarter but still 13 basis points lower than a year ago. As more recent loan vintages begin to age and as older vintages enter the foreclosure process, we may see volatility in FHA delinquency and foreclosure rates.”

While only 40% of loans serviced are in judicial states, these states account for a growing majority of loans in foreclosure, Walsh said. For states where the judicial process is more frequently used, 3.41% of loans serviced were in the foreclosure process, compared to 1.15% in non-judicial states. States that utilize both judicial and non-judicial foreclosure processes had a foreclosure inventory rate closer that of the non-judicial states at 1.36%.

“Legacy loans continued to account for the majority of all troubled mortgages. 73% of the loans that were seriously delinquent, either more than 90 days delinquent or in the foreclosure process were originated before 2008, even as the overall rate of serious delinquencies for those cohorts decreased,” she said.